-

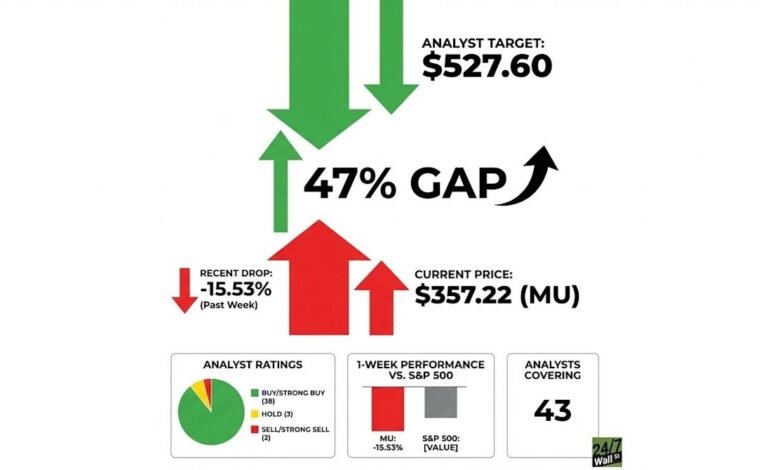

Micron (MU) is trading at $357.22 against a $527.60 consensus price target, a 47% gap, while 38 of 43 analysts rate the stock Buy or Strong Buy. The company is guiding to $33.5B in Q3 FY2026 revenue and 67% gross margin, with HBM4 memory for Nvidia’s Vera Rubin platform in mass production and calendar 2026 HBM supply fully sold out. Lam Research (LRCX) fell 9.4% on the same day that triggered the sector selloff.

-

Google’s TurboQuant algorithm announcement spooked memory investors into a fear trade, but the selloff appears to overshoot the actual risk since efficiency gains from algorithms typically expand total AI adoption and memory demand rather than permanently shrink it.

-

A recent study identified one single habit that doubled Americans’ retirement savings and moved retirement from dream, to reality. Read more here.

Micron Technology (NASDAQ: MU) is trading at $357.22, while the Wall Street consensus price target sits at $527.60. That gap of roughly 47% demands a clear-eyed look at what created it and whether it represents real opportunity or a warning sign dressed up as a bargain.

Micron is the only U.S.-based manufacturer of DRAM and a primary U.S. manufacturer of NAND memory chips, making it a central player in the AI infrastructure buildout. CEO Sanjay Mehrotra has described the company as “one of the semiconductor industry’s biggest enablers of AI,” and the financial results have backed that claim. The stock is up 291.9% over the past year. Last week changed everything.

The catalyst for the recent drop was a fear trade. On March 24, Google announced its TurboQuant algorithm, which significantly reduces memory usage in AI workloads. The announcement triggered a sharp sell-off in memory stocks, with Lam Research (NASDAQ: LRCX) dropping 9.4% the same day. Micron fell 15.5% over the past week and 13.4% over the past month.

Read: Data Shows One Habit Doubles American’s Savings And Boosts Retirement

Most Americans drastically underestimate how much they need to retire and overestimate how prepared they are. But data shows that people with one habit have more than double the savings of those who don’t.

The concern: if AI models need less memory per workload, the demand supercycle driving Micron’s revenue growth could be smaller than expected. Investors began reevaluating memory pricing and AI-driven demand assumptions almost immediately. The selloff was sector-wide, not company-specific, which matters when assessing whether the punishment fits the crime.

Wall Street is largely unmoved. Of 43 analysts covering Micron, 38 rate it Buy or Strong Buy, while just three rate it Hold and two rate it Sell. J.P. Morgan maintains a $550 price target with a Buy rating, based on the bull case resting on fundamentals that TurboQuant does not actually invalidate.

Revenue has run from $8.053 billion in Q2 FY2025 to $23.86 billion in Q2 FY2026, with Q3 FY2026 guidance calling for $33.5 billion. GAAP gross margin has expanded from 36.8% to 56.0% and is guided to 67.0% next quarter. Mehrotra has stated that “the entire calendar 2026 HBM supply, including Micron’s industry-leading HBM4,” is already sold out on price and volume. Separately, HBM4 memory designed for Nvidia’s Vera Rubin platform entered mass production in late March. Analysts also counter that efficiency gains from algorithms like TurboQuant tend to expand AI adoption broadly, ultimately increasing total memory demand.

-

Current Price: $357.22

-

Analyst Consensus Target: $527.60

-

Implied Upside: approximately 47%

-

Analysts Covering: 43

-

Buy/Strong Buy: 38

-

Hold: 3

-

Sell/Strong Sell: 2

-

1-Week Performance: −15.5%

-

YTD Performance: +25.2%

-

Trailing P/E: 17x

-

Forward P/E: 7x

-

52-Week High: $471.34

The forward multiple of 7x is striking for a company guiding to record revenue, record EPS, and record free cash flow. The PEG ratio of 0.4 suggests the market is pricing in significant deceleration that the company’s own guidance does not support. A 38-to-2 buy-to-sell ratio on a stock this widely covered carries real weight.

The fundamentals are intact. HBM4 is in mass production for Nvidia, the 2026 supply book is closed, and management has guided for record results across every major metric. A stock trading at 7x forward earnings with that momentum is priced for disaster, not for the business Micron is currently running.

The bear case centers on one real risk: if efficiency algorithms like TurboQuant represent a structural shift rather than a one-time headline, the demand forecasts underpinning both management guidance and analyst targets could prove too optimistic. Memory is a cyclical industry with heavy capital requirements. Micron plans to spend approximately $25 billion in capex in fiscal 2026. A demand air pocket at that spending level would be painful. Insider selling activity adds a small caution flag as well.

The selloff looks like a fear trade that overshot the actual risk. Analyst price targets are not guarantees, and the $527.60 consensus reflects expectations that still need to be earned. But the gap between current price and underlying business performance is wide enough that the weight of evidence leans toward opportunity, not a trap.

Most Americans drastically underestimate how much they need to retire and overestimate how prepared they are. But data shows that people with one habit have more than double the savings of those who don’t.

And no, it’s got nothing to do with increasing your income, savings, clipping coupons, or even cutting back on your lifestyle. It’s much more straightforward (and powerful) than any of that. Frankly, it’s shocking more people don’t adopt the habit given how easy it is.